Our Model Portfolios

Our model portfolios are risk-calibrated and globally diversified. Each portfolio is constructed of low-cost exchange traded funds (ETFs) that cover a broad range of equity styles plus fixed income (short-term to intermediate-term bonds). We prefer passive over actively managed funds because of their superiority in cost efficiency and performance over the long term (on a net-of-fee and risk-adjusted basis). This strategy is confirmed by the latest S&P Indices Versus Active Funds Scorecard which states that over the last 15 years 88.97% of all domestic equity funds, 91.62% of large-cap domestic equity funds, 92.71% of mid-cap domestic equity funds, 96.73% of small-cap domestic equity funds, and 89.83 % of international equity funds trailed their respective benchmarks.)

Under certain market conditions, we will purchase index put options on a broad stock market index to protect plan participants from catastrophic losses.

Definition of an Exchange Traded Fund: An ETF, or exchange traded fund, is a marketable security that tracks an index, a commodity, bonds, or a basket of assets like an index fund. Unlike mutual funds, an ETF trades like a common stock on a stock exchange. ETFs experience price changes throughout the day as they are bought and sold.

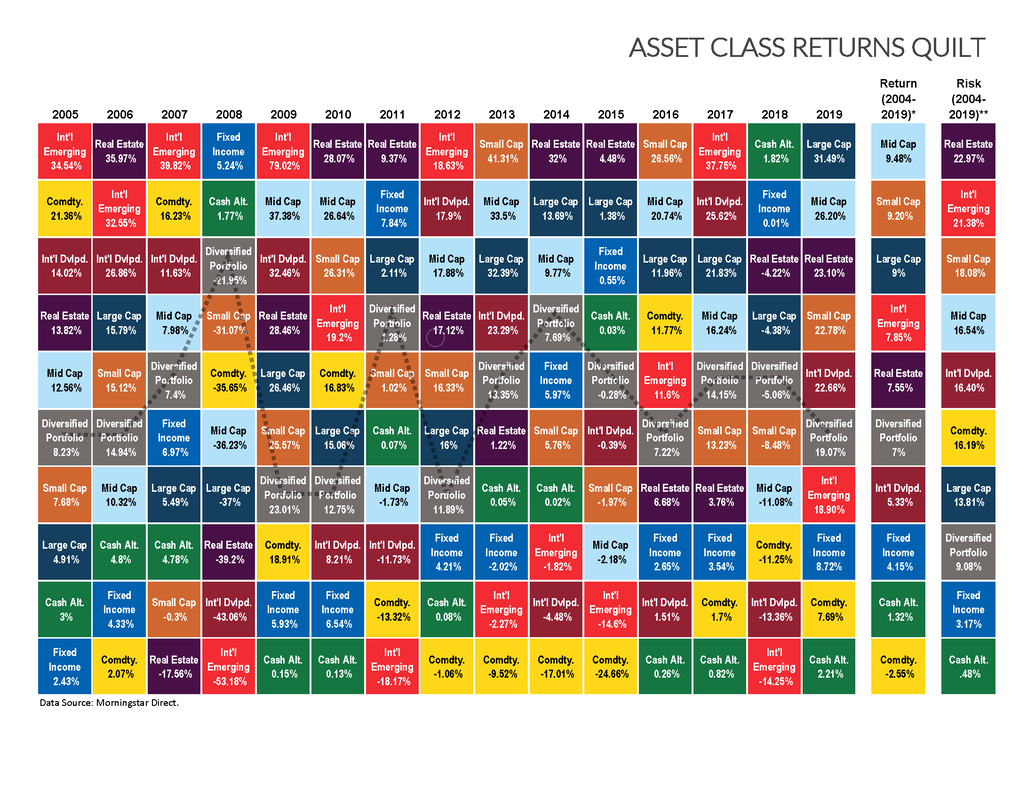

It should be noted that the ETFs selected for our model portfolios track very broad, well diversified indices covering multiple sectors. They are not sector ETFs, and we are not sector rotators. The chart below shows the difficulty in guessing which sectors will produce above average returns from one year to the next. For example, Cash Alternatives were the top performing sector in 2018 (1.82%) and the worst performing sector in 2019 (2.21%). International Emerging Stocks were the top performing sector in 2017 (37.75%) and the worst performing sector in 2018 (-14.26%).

Our model portfolios are risk-calibrated and globally diversified. Each portfolio is constructed of low-cost exchange traded funds (ETFs) that cover a broad range of equity styles plus fixed income (short-term to intermediate-term bonds). We prefer passive over actively managed funds because of their superiority in cost efficiency and performance over the long term (on a net-of-fee and risk-adjusted basis). This strategy is confirmed by the latest S&P Indices Versus Active Funds Scorecard which states that over the last 15 years 88.97% of all domestic equity funds, 91.62% of large-cap domestic equity funds, 92.71% of mid-cap domestic equity funds, 96.73% of small-cap domestic equity funds, and 89.83 % of international equity funds trailed their respective benchmarks.)

Under certain market conditions, we will purchase index put options on a broad stock market index to protect plan participants from catastrophic losses.

Definition of an Exchange Traded Fund: An ETF, or exchange traded fund, is a marketable security that tracks an index, a commodity, bonds, or a basket of assets like an index fund. Unlike mutual funds, an ETF trades like a common stock on a stock exchange. ETFs experience price changes throughout the day as they are bought and sold.

It should be noted that the ETFs selected for our model portfolios track very broad, well diversified indices covering multiple sectors. They are not sector ETFs, and we are not sector rotators. The chart below shows the difficulty in guessing which sectors will produce above average returns from one year to the next. For example, Cash Alternatives were the top performing sector in 2018 (1.82%) and the worst performing sector in 2019 (2.21%). International Emerging Stocks were the top performing sector in 2017 (37.75%) and the worst performing sector in 2018 (-14.26%).

Our ETF Evaluation Process (initial and Ongoing)

ETFs have exploded in popularity over the past few years. There are many types of ETFs and one can be found to meet almost any need. But there are legitimate concerns about investing in ETFs: 1) the vast majority of ETFs on the market today have very short histories (track records); and 2) unlike mutual funds, ETFs are very complex investment instruments. It’s unfortunate, but many investors buy them, and many advisors recommend them, without fully understanding the complexities that exist with these investment vehicles.

But, there are three distinct advantages to ETF investing. The first is liquidity. Since ETFs trade like an equity on an exchange, they can be bought and sold at any time the exchange is open (open-ended mutual funds can only be purchased or redeemed at the close of each business day). A second advantage is that ETFs, on average, have lower expense ratios than index mutual funds. The third advantage involves transparency. Unlike mutual funds, the holdings of an ETF can be viewed on a daily basis.

We have developed a very regimented and consistent process for evaluating the ETFs that will be selected for our model portfolios. First, we prefer ETFs with long track records (most have been in existence for more than 10 years). Second, they must track very broad, well diversified indices covering multiple sectors. Third, they must consistently produce very low tracking errors.

Risk Measures That We Compute Each Quarter In Our ETF Evaluation Process

How We Construct Our Portfolios

Our model portfolios are designed to be mean-variance efficient along a Markowitz Efficient Frontier. This simply means that they produce the highest return possible for their level of risk exposure (optimization).

But, the optimization of portfolios is not an exact science. Results are dependent on the input data used. We believe that we add value by taking the time to add carefully thought-out inputs into the optimization process, as opposed to blindly using the historical inputs that exist in a software application, or by arbitrarily overriding the historical inputs with a forecasting guess.

We use historical averages over known market cycles to help us determine what a reasonable estimate of returns should be, and we take into account the convergence of correlations that occur when markets decline. We also use recent, not ancient-historical inputs, and we don’t impose an arbitrarily fabricated forecast based on our emotional state.

ETFs have exploded in popularity over the past few years. There are many types of ETFs and one can be found to meet almost any need. But there are legitimate concerns about investing in ETFs: 1) the vast majority of ETFs on the market today have very short histories (track records); and 2) unlike mutual funds, ETFs are very complex investment instruments. It’s unfortunate, but many investors buy them, and many advisors recommend them, without fully understanding the complexities that exist with these investment vehicles.

But, there are three distinct advantages to ETF investing. The first is liquidity. Since ETFs trade like an equity on an exchange, they can be bought and sold at any time the exchange is open (open-ended mutual funds can only be purchased or redeemed at the close of each business day). A second advantage is that ETFs, on average, have lower expense ratios than index mutual funds. The third advantage involves transparency. Unlike mutual funds, the holdings of an ETF can be viewed on a daily basis.

We have developed a very regimented and consistent process for evaluating the ETFs that will be selected for our model portfolios. First, we prefer ETFs with long track records (most have been in existence for more than 10 years). Second, they must track very broad, well diversified indices covering multiple sectors. Third, they must consistently produce very low tracking errors.

Risk Measures That We Compute Each Quarter In Our ETF Evaluation Process

- Excess Return: Fund return – Benchmark (index) return

- Tracking Error: Annualized standard deviation of quarterly excess returns over various trailing time periods

- Standard Deviation Compared to the Benchmark (index): Standard deviation is the square root of the variance. In simpler terms, standard deviation is a measure of how much an investment’s (or portfolio’s) returns can vary from its average return. It is a measure of volatility and in turn, risk.

- Value at Risk (VaR) Compared to the Benchmark (index): A measure of risk that estimates how much a portfolio might lose, given normal market conditions, in a set time period.

- Factor Analysis of the Fund: Quantitative analysis allowing for the capture of those historical risk factors that have appropriately compensated investors for risks taken, including market, size, value, and momentum for equities, and term and default for fixed income instruments.

How We Construct Our Portfolios

Our model portfolios are designed to be mean-variance efficient along a Markowitz Efficient Frontier. This simply means that they produce the highest return possible for their level of risk exposure (optimization).

But, the optimization of portfolios is not an exact science. Results are dependent on the input data used. We believe that we add value by taking the time to add carefully thought-out inputs into the optimization process, as opposed to blindly using the historical inputs that exist in a software application, or by arbitrarily overriding the historical inputs with a forecasting guess.

We use historical averages over known market cycles to help us determine what a reasonable estimate of returns should be, and we take into account the convergence of correlations that occur when markets decline. We also use recent, not ancient-historical inputs, and we don’t impose an arbitrarily fabricated forecast based on our emotional state.